Dr. Vikas Bhardwaj

India in May 2026 inhabits a world of simultaneous strategic opportunity and fiscal peril. The Economic Survey 2025–26 projects real GDP growth of 7.4% for FY2026, with private final consumption expenditure at 61.5% of GDP — the highest since 2011–12. India has received three sovereign credit rating upgrades in 2025, from Morningstar DBRS, S&P Global Ratings, and R&I, validating the Union government's fiscal consolidation path. Central fiscal deficit has been compressed from 9.2% of GDP in FY2021 to a budgeted 4.4% in FY2026. Major central subsidies fell from 1.9% of GDP in FY2022 to 1.2% in FY2025, aided by Direct Benefit Transfers.

Against this disciplined central backdrop, India's states have drifted toward a fiscal arms race. The Russia–Ukraine war, now in its fourth year, has restructured global energy markets and supply chains. The Red Sea crisis has added 15–20 days and significant freight costs to Asia–Europe trade routes. China's 2025 defence budget surged to USD 245 billion — approximately 3.4 times India's allocation of Rs 6.81 lakh crore (1.9% of GDP). China's provincial governments compete to attract industrial investment; India's state governments increasingly compete to distribute free electricity. Post–Operation Sindoor (May 2025), India's strategic reality demands defence modernisation, semiconductor sovereignty, and AI infrastructure at a scale fundamentally incompatible with institutionalised fiscal irresponsibility at the subnational level.

India's national R&D expenditure stands at 0.64% of GDP (Economic Survey 2025–26) — compared with South Korea's 4.9%, Israel's 6.0%, and China's 2.4%. Every rupee diverted to financing a politically timed, unconditional cash transfer is a rupee not invested in AI infrastructure, semiconductor fabrication, logistics modernisation, or the defence capabilities that post–Operation Sindoor India urgently requires.

2. The Analytical Distinction: Welfare Economics vs. Revdi Culture

Welfare economics, from Musgrave's tripartite theory of public finance to Samuelson's merit goods framework and Stiglitz's work on externalities, provides a rigorous basis for distinguishing productive welfare from distortive freebies. Merit goods — primary education, preventive healthcare, nutritional support for children — generate positive externalities, enhance the production possibility frontier, and pass the market-failure test. They are justified on allocative, distributive, and stabilisation grounds simultaneously.

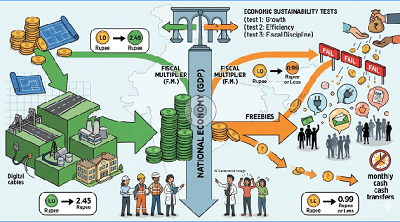

Distortive freebies — universal free electricity regardless of income, politically timed loan waivers, and monthly cash transfers without conditionality or sunset clauses — fail all three tests. Research by Bose and Bhanumurthy (NIPFP, 2013, 2015) establishes that infrastructure capital expenditure carries a fiscal multiplier of 2.45: each rupee invested generates Rs 2.45 in GDP. Untargeted subsidies carry multipliers of 0.99 or less. The opportunity cost is not theoretical — it is Rs 1.45 lakh crore in foregone GDP for every Rs 1 lakh crore reallocated from capex to unconditional transfers.

3. 1 Himachal Pradesh: The Most Urgent Warning Signal

Himachal Pradesh's fiscal trajectory embodies every pathology this paper describes. A small, mountainous state with a narrow revenue base and structurally high committed expenditure, it ran revenue surpluses between 2018–19 and 2021–22, supported by generous Revenue Deficit Grants from the 15th Finance Commission. The state's political class — Congress and BJP alternating power every five years — treated these grants not as a fiscal cushion to build reserves, but as a licence to expand expenditure: salaries, pensions, subsidies, and political appointments, all without structural revenue reform.

When the 15th Finance Commission's RDG was tapered to near-zero in FY2026 (a schedule publicly announced from 2021), Himachal Pradesh faced a fiscal cliff it had done nothing to avoid. Economists and media commentators — including The New Indian Express and Times of India reports — describe conditions increasingly resembling near-insolvency: deferred salaries, a shrinking development budget, and capital outlay slashed by 55%. It bears emphasis: Himachal Pradesh has not formally declared bankruptcy — Indian states have no mechanism to do so — but analysts, CAG auditors, and senior state officials themselves now use language that suggests a structural solvency stress that is qualitatively different from normal fiscal difficulty.

The CAG's warning from 2017 was precise: Himachal Pradesh would enter a debt trap by 2018–19, with liabilities already at 176% of revenue receipts. Nine years later, the warning has been not merely confirmed but exceeded. The lesson is systemic: when bipartisan competitive populism meets a structural revenue constraint, fiscal collapse is not a risk — it is an arithmetic certainty.

3.2 Punjab: The Anatomy of a Debt Trap

Punjab's power subsidy — initiated in 1997 for small landholders, expanded universally by each successive government — has grown from Rs 5,059 crore (2012–13) to Rs 21,000+ crore today. The AAP government's promise of 300 units free electricity added an estimated Rs 14,337 crore to annual subsidy costs (PFC / Power Ministry estimates). PSPCL is owed Rs 10,000 crore in unpaid subsidy arrears and Rs 3,600 crore in unpaid government department bills — off-budget liabilities that do not appear in official debt statistics but represent real fiscal obligations. Groundwater depletion from unmetered free agricultural power compounds the economic damage with an irreversible agricultural crisis. Free power has become Punjab's most expensive political product.

The macroeconomic pathology of competitive populism operates through six well-established transmission mechanisms that collectively represent a structural threat to India's long-term fiscal stability and strategic capacity.

4.1 The Crowding-Out Effect and Capital Formation Crisis

The RBI has explicitly documented that states' market borrowings rose 21% year-on-year in the first half of FY2026, directly pushing up government bond yields and reducing borrowing space for both the Centre and the private sector. Karnataka's CAG report (August 2025) provides the clearest micro-level evidence: five guarantee schemes consuming Rs 52,000 crore triggered a revenue deficit of Rs 9,271 crore, required Rs 63,000 crore in net market loans (Rs 37,000 crore above prior year), reduced capital expenditure by Rs 5,229 crore, and caused incomplete infrastructure projects to surge by 68%. The fiscal multiplier mathematics is unambiguous: Karnataka's guarantees generated a multiplier of approximately 0.99, while the foregone capital expenditure would have generated 2.45x in GDP.

4.2 DISCOM Liabilities: The Hidden Fiscal Iceberg

National DISCOM outstanding debt stood at Rs 7.42 lakh crore (2.7% of GDP) as of March 2024, per Power Finance Corporation data cited in the existing analysis. When state governments promise free electricity but fail to transfer subsidy reimbursements to distribution companies, DISCOMs borrow commercially — accumulating debt that does not appear in state budgets but represents real taxpayer obligations. Punjab's PSPCL alone carries Rs 13,600 crore in direct receivables from the state, with Rs 31,122 crore in irrevocable state guarantees. This is India's version of Pakistan's energy circular debt — a structural pathology that grows in the dark until it crystallises into a fiscal emergency.

5. The Global Graveyard of Fiscal Populism

History provides a clear-eyed verdict on governments that institutionalise debt-financed consumption redistribution at the expense of productive investment. The cases below are not abstractions — they are the documented fiscal autopsies of nations that made the choices India's states are currently making.

Public choice theory explains with clinical precision why competitive populism persists despite its evident macroeconomic costs. Electoral cycles in India are continuous — with some state election almost every year. Politicians face a structural principal-agent problem: voters (principals) have difficulty connecting today's free electricity to tomorrow's debt burden; politicians (agents) face strong incentives to promise short-term visible benefits while costs are diffuse, delayed, and borne by future taxpayers who cannot yet vote. No party can unilaterally disarm from the freebie race without surrendering electoral ground — a collective action problem with no internal solution.

This dynamic is politically agnostic. BJP-led states have deployed targeted welfare announcements — Ladli Behna (Madhya Pradesh), various pre-election transfers in Rajasthan and Chhattisgarh. Congress's Karnataka Five Guarantees and AAP's free electricity in Punjab and Delhi represent the apex of the institutional freebie model. DMK's Tamil Nadu and TMC's West Bengal have entrenched welfare architectures built over decades. The critique is structural, not partisan: wherever fiscally irresponsible populism appears, regardless of political colour, it imposes the same macroeconomic costs.

The evidence assembled in this analysis admits no comfortable ambiguity. Sixteen Indian states have breached their FRBM fiscal deficit ceilings. States' unconditional cash transfers have reached Rs 1.7 lakh crore annually — sufficient to fund India's entire National Health Mission nearly five times over. Punjab is enmeshed in a textbook debt trap, with 86% of new borrowings consumed by old debt repayment. Himachal Pradesh's budget has shrunk for the first time in modern history, its Chief Minister has deferred his own salary, and economists and media commentators describe conditions increasingly suggestive of near-insolvency. Karnataka's CAG has documented a direct causal link between guarantee expenditure, capital contraction, and project incompletion. The DISCOM debt iceberg — Rs 7.42 lakh crore nationally — mirrors the dynamics that destroyed Lebanon's Electricité du Liban and Pakistan's power sector, at scale.

The international comparisons are equally unambiguous. Greece, Lebanon, Sri Lanka, Argentina, Pakistan, and Venezuela each institutionalised versions of what India's states are now practising: debt-financed consumption subsidies that prioritised short-term political payoffs over long-term productive investment. Each paid a catastrophic price — sovereign default, hyperinflation, GDP collapse, social crisis, or IMF-supervised adjustment that imposed on citizens a multiple of the pain the original subsidies had been designed to prevent. Germany, Sweden, South Korea, and Singapore demonstrate the alternative: welfare grounded in productivity, conditionality, taxation capacity, and institutional discipline — welfare that builds human capital rather than consuming it.

Post–Operation Sindoor, India faces a security environment demanding defence modernisation at a pace that requires 3% of GDP, not 1.9%. China's defence budget is 3.4 times India's. China's R&D spending is 2.4% of GDP; India's is 0.64%. China's provinces compete on industrial parks; India's states compete on free electricity units. This asymmetry, if uncorrected, will determine whether India captures the China Plus One supply-chain opportunity or cedes it to Vietnam, Malaysia, and Indonesia.

KEY INSTITUTIONAL SOURCES

( Dr. Vikas Bhardwaj Ph.D. & M.Phil., Centre for Russian & Central Asian Studies, School of International Studies, Jawaharlal Nehru University, New Delhi)

(The content of this article reflects the views of writer and contributor, not necessarily those of the publisher and editor. All disputes are subject to the exclusive jurisdiction of competent courts and forums in Delhi/New Delhi only)

Leave Your Comment