Dr Vikas Bhardwaj

On 22 June 2026, the Ministry of Home Affairs notified the Foreign Contribution (Regulation) Amendment Rules, 2026 (Ministry of Home Affairs, 2026). Eight days later, Union Home Minister Amit Shah launched the accompanying FCRA 2.0 digital portal (Press Information Bureau, 2026); the day after that, the Kerala Legislative Assembly voted 111 to 2 to demand both be withdrawn (Kerala Legislative Assembly, 2026). Those events, compressed into ten days, frame the question this brief answers: not whether foreign funding should be regulated — nearly every democracy regulates it — but whether India’s 2026 framework, and specifically its exclusion of proselytisation from fundable religious activity, is a proportionate evolution of an existing regime or a step beyond it.

The New Logic of Strategic Sovereignty

India has treated this question less as settled policy than as a ratchet, adding a layer of scrutiny in nearly every decade since the original 1976 Act. What sets 2026 apart is the level at which scrutiny now operates. Earlier amendments asked who was receiving foreign money and through which bank account; the 2026 Rules ask what the money may be spent on, tied to a closed schedule of purposes and to the states where an association may operate (Ministry of Home Affairs, 2026). That is a move from financial oversight to activity licensing, reinforced institutionally by the new FCRA 2.0 portal, which integrates the regulatory database with PAN, Aadhaar, OCI and bank records (Press Information Bureau, 2026).

A regime built around disclosure and audit is a familiar, largely uncontroversial form of regulation. A regime that also requires an organisation to select its activities from a government-drafted list, disclose office-bearers’ social media accounts, and lose religious-category eligibility altogether if its work strays into proselytisation is doing something more: defining, in advance, what a foreign-funded religious or charitable life in India may look like. Whether that additional layer is proportionate to the harm it targets is the question this brief answers with evidence.

The argument here is that the 2026 Rules are best read as continuation rather than rupture: they extend a regulatory logic the Supreme Court has already tested, targeting a specific, previously under-defined problem — inducement-based conversion financed from abroad — rather than religious practice broadly. That reading holds up well against the doctrinal record; it holds up less comfortably against the still-pending Bill’s proposal to let an executive authority take control of an association’s assets, which raises proportionality questions neither Parliament nor the courts have yet resolved.

From Financial Oversight to National Security

The securitisation of this policy area did not begin in 2026. In Noel Harper v. Union of India (2022), the government argued that foreign inflows had roughly doubled between 2010 and 2019 and that some contributions had financed activity of security concern; the three-judge Supreme Court bench accepted that framing, holding that foreign contribution can materially affect the country’s social and political fabric and that its presence ought to be kept at a minimum (Supreme Court of India, 2022; Supreme Court Observer, 2022). The Court drew a distinction that still structures the law: forming an association is a fundamental right under Article 19, but receiving foreign contribution for it is not — it is a regulated privilege, revocable on public-interest grounds (Supreme Court of India, 2022).

That reasoning has a precedent older than the current government. In 2012, after Prime Minister Manmohan Singh publicly blamed foreign-funded, largely US- and Scandinavia-based NGOs for stalling the Kudankulam nuclear plant, the Home Ministry moved against groups including the Tuticorin Diocesan Association and the Tuticorin Multipurpose Social Service Society on suspicion that foreign funds were being diverted to the protests (Indian Express, 2012). The 2026 Rules institutionalise, at rule-making level, an executive instinct toward treating foreign funding as a security variable that predates the present government by well over a decade.

Administratively, the 2026 Rules extend that instinct through the expanded “key functionary” definition, which closes a governance gap that let foreign nationals or unaccountable office-bearers direct an association’s affairs, and through purpose- and geography-linked registration, which lets the state track not just how much money enters the country but what happens to it afterward (Ministry of Home Affairs, 2026). Registration data illustrate the scale: roughly 14,500 associations hold active FCRA status today, against a cumulative 21,933 whose licences have lapsed or been cancelled since 1976 — up from 20,701 as recently as April 2024 (Business Standard, 2024; Amnesty International India, 2026; Press Information Bureau, 2026).

Drawing the Line on Foreign-Funded Proselytisation

The Rules’ most distinctive feature is the religious-purpose schedule. It does not eliminate categories such as religious education or preservation of tradition; it enumerates specific permitted religious activities and expressly excludes proselytisation from that list (Ministry of Home Affairs, 2026). The line being drawn is not between religion and secular life, but between propagating belief through the exposition of its tenets and pursuing conversion through foreign-financed inducement.

That distinction sits inside a larger domestic architecture. Twelve of India’s twenty-eight states now enforce their own Freedom of Religion statutes, with penalties ranging from one year’s imprisonment to ten years in the most stringent laws (USCIRF, 2025). For the first time, the 2026 Rules align foreign-funding regulation directly with the constitutional line these state laws already draw: propagation of belief is protected, conversion by force, fraud or inducement is not (Supreme Court of India, 1977).

The strategic point of enumerating the schedule this way is to close a regulatory arbitrage that critics and officials alike have long identified — conversion-linked expenditure booked under broad headers such as “religious education” — by converting an open-ended administrative judgment into something closer to a fixed statutory boundary, even if an interpretively contestable one. Whether that reduces discretion or simply relocates it is exactly the question the Kerala Assembly raises, taken up below.

Balancing Religious Freedom with Regulatory Accountability

The constitutional terrain is layered. Article 19(1)(c) guarantees the freedom to form associations, subject under Article 19(4) to reasonable restrictions for sovereignty, integrity and public order. Article 25 guarantees freedom of conscience and the right to profess, practise and propagate religion, subject to public order, morality and health; Article 26 separately protects a religious denomination’s right to manage its own affairs. Article 300A, protecting property from deprivation except by authority of law, becomes directly relevant to the pending Bill’s proposal for a Designated Authority empowered to take control of, and in some cases dispose of, assets built from foreign contribution once a registration lapses or is cancelled.

Two decisions anchor this analysis. In Rev. Stainislaus v. State of Madhya Pradesh (1977), a five-judge Constitution Bench read “propagate” in Article 25(1) to mean transmitting belief through exposition of its tenets, held the Article confers no right to convert another person, and upheld state anti-conversion statutes as legitimate public-order legislation (Supreme Court of India, 1977). The 2026 Rules’ conversion carve-out draws on the same distinction, applied through funding regulation rather than criminal law. In Noel Harper (2022), the Supreme Court upheld the core 2020 amendments — the sub-granting ban, the single designated bank account and Aadhaar-based identification — holding there is no fundamental right to receive foreign contribution (Supreme Court of India, 2022). Commentators have argued this reasoning under-applies the proportionality test that ordinarily governs Article 19 restrictions, a critique likely to resurface if the 2026 Rules face challenge (Supreme Court Observer, 2022).

Lessons from Other Democracies

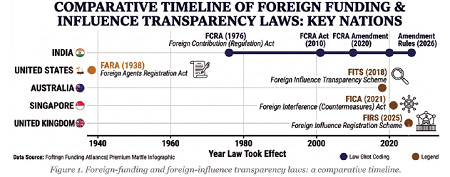

FARA in the United States, FITS in Australia, and the United Kingdom’s newly operational Foreign Influence Registration Scheme are disclosure-based regimes aimed narrowly at political-influence activity for a foreign government or political principal, and each carries explicit or effective exemptions for charitable, humanitarian and religious work, because the mischief they address is covert political lobbying, not philanthropic funding (U.S. Department of Justice, 1938; Government of Australia, 2018; Government of the United Kingdom, 2023). Singapore’s Foreign Interference (Countermeasures) Act targets hostile information campaigns and the designation of “politically significant persons,” and is deliberately looser than the American or Australian models, reflecting Singapore’s dependence on external engagement (Government of Singapore, 2021).

India’s FCRA framework departs from that pattern in one structurally important way: rather than confining itself to political-influence activity, it regulates the entire field of foreign-funded civil society — social, economic, educational, cultural and religious — as a single area of national-security concern (Ministry of Home Affairs, 2026). That is the real comparative lesson. Most peer democracies target political and lobbying activity narrowly while carving charitable and religious work out of scope; India’s 2026 Rules instead bring charitable and religious funding inside the perimeter of purpose-based oversight, paired with a proposed asset-vesting power none of the four comparator regimes possesses. That breadth is defensible given the far larger scale of India’s foreign-funded civil-society sector than the lobbying ecosystems FARA or FITS were built for, but it also explains why India’s regime provokes a category of objection — about charitable and religious autonomy specifically — that barely registers in the Western transparency-scheme literature, where charities are typically exempted rather than regulated.

Protecting Civil Society Without Compromising Sovereignty

The strongest counterarguments deserve to be stated in full. Amnesty International India has cited official figures showing 21,933 organisations had lost their FCRA licences as of March 2026, disproportionately affecting groups working in minority rights, free expression and environmental action (Amnesty International India, 2026). On 1 July 2026 the Kerala Legislative Assembly passed, 111 votes to two, a resolution asking the Centre to withdraw both the pending Bill and the notified Rules, arguing the framework strains Articles 19 and 25, cuts against federalism, and — most relevant here — leaves “proselytisation” undefined in a way that could be turned against organisations serving tribal and vulnerable communities (Kerala Legislative Assembly, 2026).

The objections are not confined to India. Senator James Risch, chairman of the US Senate Foreign Relations Committee, has called the framework deeply concerning and warned that using FCRA to expand pressure on US-linked Christian ministries through asset seizure would trouble the bilateral relationship; Democratic congressional aides have separately said Congress is watching the asset-vesting provision on a bipartisan basis, and Congressman Chris Smith urged Secretary of State Marco Rubio to raise the issue during his India visit (Hindustan Times, 2026). The Catholic Bishops’ Conference of India has described the amendments as dangerous and alarming (Bhatt & Joshi Associates, 2026).

None of this can be dismissed as mere inconvenience — a standard the Supreme Court itself declined to accept in Noel Harper even while letting the 2020 amendments proceed (Supreme Court of India, 2022). The government’s position, consistent since 2020, is that the changes impose no blanket prohibition, that exemption and review mechanisms exist, and that the tightening follows demonstrated misuse. Still missing from the public record is transparent data on how much cancellation activity is actually proselytisation-related, as against non-filing or non-utilisation; absent that breakdown, the proportionality of a sector-wide licensing regime remains an open empirical question rather than a settled one. The Bill itself was pulled from the Budget Session order paper on 2 April 2026 after opposition protests and still awaits the Monsoon Session, even though the Rules and the FCRA 2.0 portal — needing no fresh parliamentary vote — are already in force (Bhatt & Joshi Associates, 2026; Press Information Bureau, 2026).

The New Logic, Revisited

Return, then, to the question this brief opened with. Do India’s 2026 FCRA Rules amount to a legitimate evolution from financial regulation toward strategic sovereignty, or a disproportionate restriction on civil society? The doctrinal record supports the first reading: the Rules extend a regulatory logic the Supreme Court has already tested and a security framing that predates the current government by over a decade, targeting a specifically defined problem within the religious domain rather than religious practice as a whole. The implementation record counsels more caution: the new licensing structure’s breadth, its extension into channels like social-media disclosure, and the pending Bill’s asset-vesting powers reach further into the ordinary governance of foreign-funded civil society than any peer democracy attempts, raising proportionality questions neither Parliament nor the courts have yet settled. The 2026 Rules are, on the evidence, a genuine evolution in doctrine; whether they are also a proportionate one is a question the government’s own unpublished data, and Parliament’s still-pending Bill, leave open.

References

(The content of this article reflects the views of writer and contributor, not necessarily those of the publisher and editor. All disputes are subject to the exclusive jurisdiction of competent courts and forums in Delhi/New Delhi only)

Leave Your Comment